Gas station / convenience store properties sit in an oft-maligned corner of the net lease world. They trade all the time, yet they’re still treated like the red-headed stepchild compared to other single-tenant NNN credit retail properties.

Except for one name: 7-Eleven.

7-Eleven is the benchmark for convenience stores in the NNN investment world. That’s not news to anyone. They are the best of the best.

Rarely do you see 7-Eleven close a location. In fact, I’m sure everyone reading this article has a 7-Eleven within 10 miles of their home that has been operating for over 40 years. That kind of longevity is rare. You can’t say that about many tenants. Maybe McDonald's sits in the same category, but that’s about it.

That type of operating history gives investors comfort. There’s also the nostalgia factor. Most people buying a 7-Eleven property can probably remember getting a Slurpee in their local 7-Eleven as a kid. That familiarity has a meaningful impact whether people admit it or not.

7-Eleven’s recent (last several years) focus on opening sites with gas marked a pretty big change in their expansion strategy. I can’t recall the last time I saw a new 7-Eleven development without gas.

Sure, 7-Eleven has thousands of stores without gas and they continue to extend leases on these legacy sites, but they have clearly stated that opening new sites will require a gas component. Gas drives sales. They make plenty of money from gas, but the gas feeds the c-store as well.

7-Eleven has the biggest footprint in the country with a mix of company and franchise operated stores, and an active development pipeline that keeps new locations coming online. The brand awareness, historical operations, and national presence explains why 7-Eleven assets show up constantly in the single-tenant net lease market.

From a corporate standpoint, Seven & i Holdings Co., Ltd. continues to reinvest heavily in North America, with a focus on larger formats and food-forward stores. They’ve also been public about long-term expansion plans, which is pretty easy to see when looking at the number of new 7-Eleven sites that have come out of the ground over the last several years.

That’s all fine and dandy. I’m more interested in exploring the market perception of 7-Eleven as an investable tenant. I should also mention that tenants like Circle K, Wawa, and QuikTrip have, to a lesser extent than 7-Eleven, also benefited from elevated investor interest in the single-tenant NNN marketplace as compared to other gas station assets.

What do I mean by this? Anyone that has been in the single-tenant retail investment marketplace for more than a few years can tell you that gas station properties garner significantly less investor interest than competing single-tenant assets. This is just a fact. The buyer pool for gas stations is only a fraction of the overall NNN asset buyer pool.

The reasons the buyer pool is smaller:

I know multiple active retail NNN investors that will not buy a gas station………but they will buy a 7-Eleven with gas.

Huh?

This is a massive head-scratcher. The contradiction has been around for years, and it still doesn’t make logical sense.

I totally get not wanting to buy a net leased gas station leased to a small operator with only two or three locations. The tenant’s pockets aren't deep enough to shield the landlord from any environmental liability. I get that.

What about a corporate lease from BP, Chevron, Equilon, Shell, Mobil, etc.? Aren’t every one of those companies as big or bigger than 7-Eleven? Why the concern? Isn’t the risk of contamination from having underground tanks the same whether the station is operated by 7-Eleven or Chevron? The tanks are still underground. The risk profile is identical.

I honestly can’t answer these questions with absolute certainty. I can only speculate based on personal experience.

Here’s my hypothesis:

7-Eleven properties are not considered gas stations. I know that sounds crazy to say because if there are gas pumps in the parking lot, the property is most definitely a gas station.

As I alluded to above, people’s personal experiences with 7-Eleven stores don’t typically evoke the feeling of visiting a traditional gas station. There are no service bays or attendants with dirty hands and stained blue uniforms.

In a world where gas station properties fall under extreme investor scrutiny, 7-Eleven somehow gets a free pass. It shouldn’t, but it does.

That perception creates differentiation. One of my favorite sayings is “Perception is reality.” The reality is that the valuation gap exists. You can see it every time a 7-Eleven deal trades at a more aggressive CAP rate than competing gas / c-store assets with comparable lease terms and credit.

If you’ve got a better explanation, I’d honestly love to hear it. Whatever the reason, the market treats 7-Eleven differently, and it’s been that way for as long as I can remember.

One thing I can say for certain is that 7-Eleven’s real estate department is better than most. At no time was this more evident than several years ago when they approached loads of their developers that had signed 7-Eleven ground leases and converted them to build-to-suit leases.

7-Eleven saw the writing on the wall. Costs were rising rapidly and inflation was going to put significant pressure on every aspect of construction. The cost of capital was also rising at the same time. Keeping their leases as ground leases meant those rising construction costs would fall squarely on 7-Eleven’s shoulders. They weren’t going to let that stand so they transferred the risk to their developers.

7-Eleven approached their developers and said either the leases needed to be converted to build-to-suits or the deals were dead. Almost all of the developers agreed, thinking the increased rent would mean a higher back end value and therefore yield more profit.

When these developers struck these deals two or more years before completion, they had little idea how quickly interest rates would rise and cap rates would follow.. All those expected 150-250 basis points of spread (profit margins) evaporated by the time deals were ready to hit the market.

It was a perfect storm for developers. Rising CAP rates and increasing construction costs meant all the profit was gone.

In one final stroke of genius (or stupidity on the part of the developers), 7-Eleven was able to negotiate (in many of the converted build-to-suit leases) a provision whereby the build-to-suit rent would not be increased if the developer exceeded the agreed upon construction budget but the rent would be reduced if the developer’s final costs came in below the budget. 7-Eleven gets the benefit of lower costs (if that happens) but the developer takes all the pain of any increased costs. Brutal.

Having the best data helped 7-Eleven make savvy decisions ahead of their counterparties.

Speed to data and information always wins.

That’s where DealGround comes in.

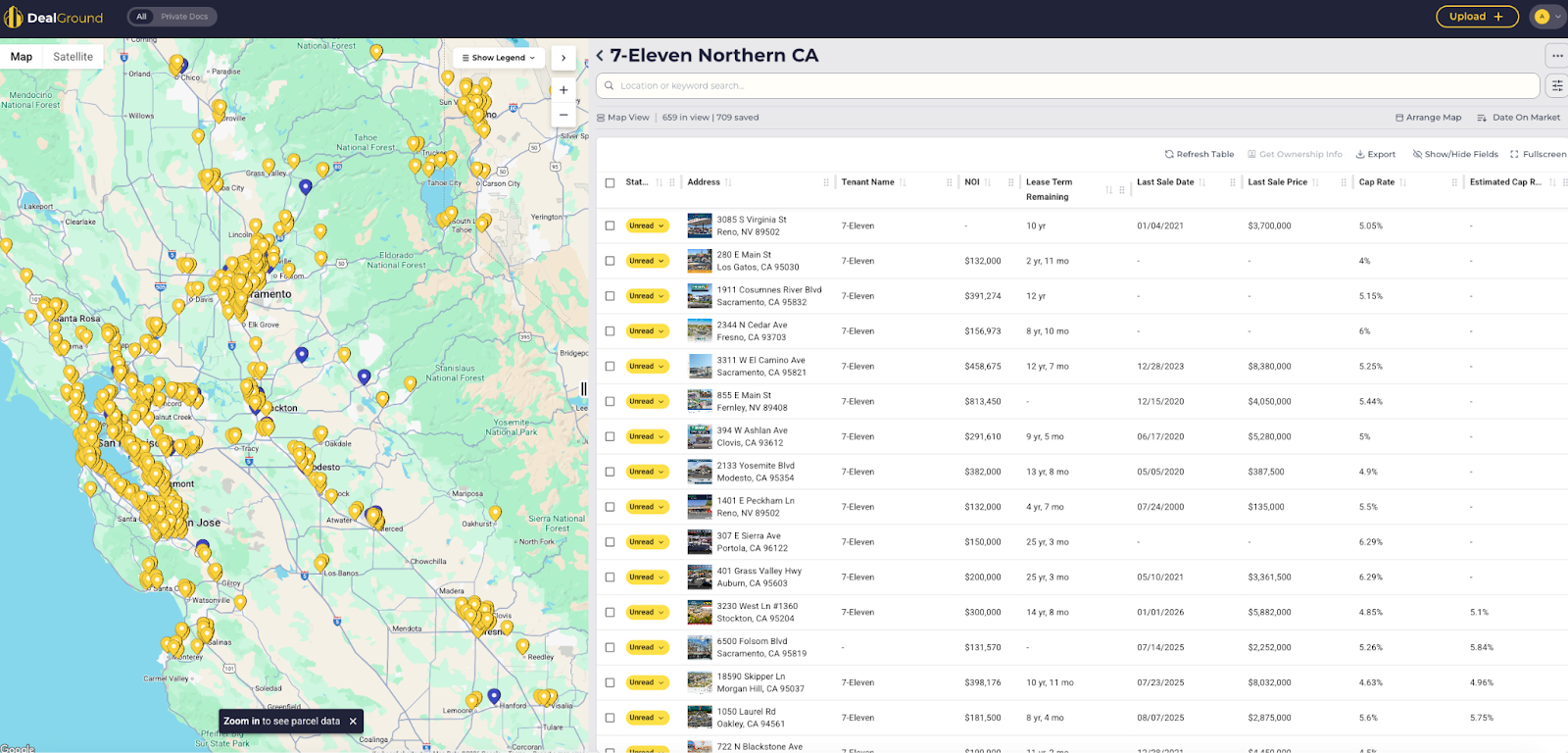

When you pull up the Northern California 7-Eleven map in DealGround (image below), the story gets even clearer. You can see historical sale transactions, actively marketed deals, actual NOI figures, and compare lease terms side by side.

Analyze the following:

It’s all visible in seconds.

Instead of guessing why one deal trades more aggressively than another, you can see it. That’s the difference. Real data. Real context. Real clarity on any market or tenant at any time.